Our AI Agent helps MGAs and carriers triage submissions, enforce appetite rules, and make faster underwriting decisions — all from your own guidelines, policies, and systems.

Enterprise-ready security • Auditable decisions • Human-in-the-loop

Faster submission triage.

Consistent appetite enforcement.

Underwriters focus on deals, not searching.

Scale capacity without adding headcount.

Book a demo to see the difference!!!

See how underwriting teams make faster, more consistent decisions.

Book demo

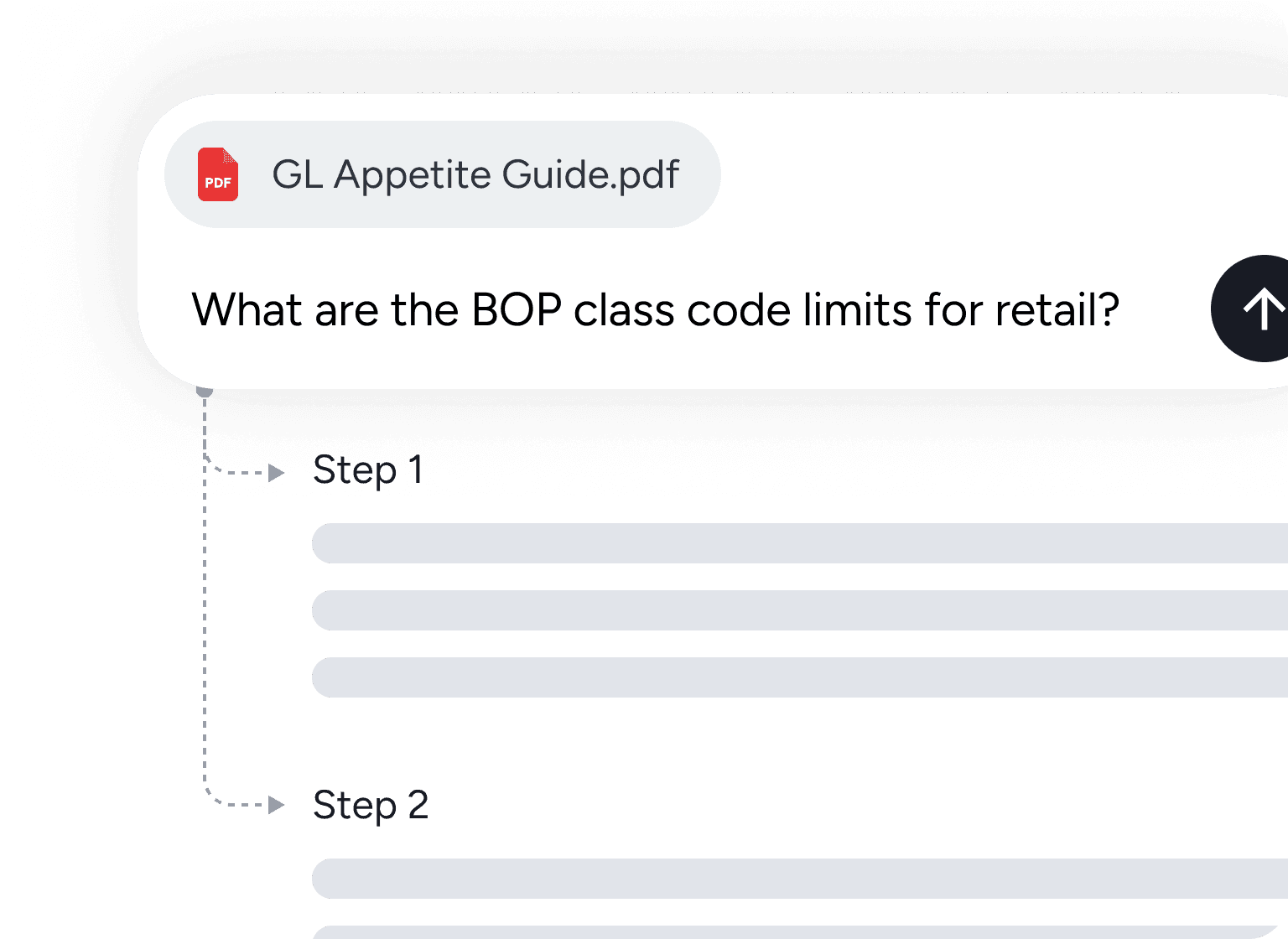

Every answer cites your source documents.

Works only with your firm's data and guidelines.

Built specifically for regulated insurance operations.

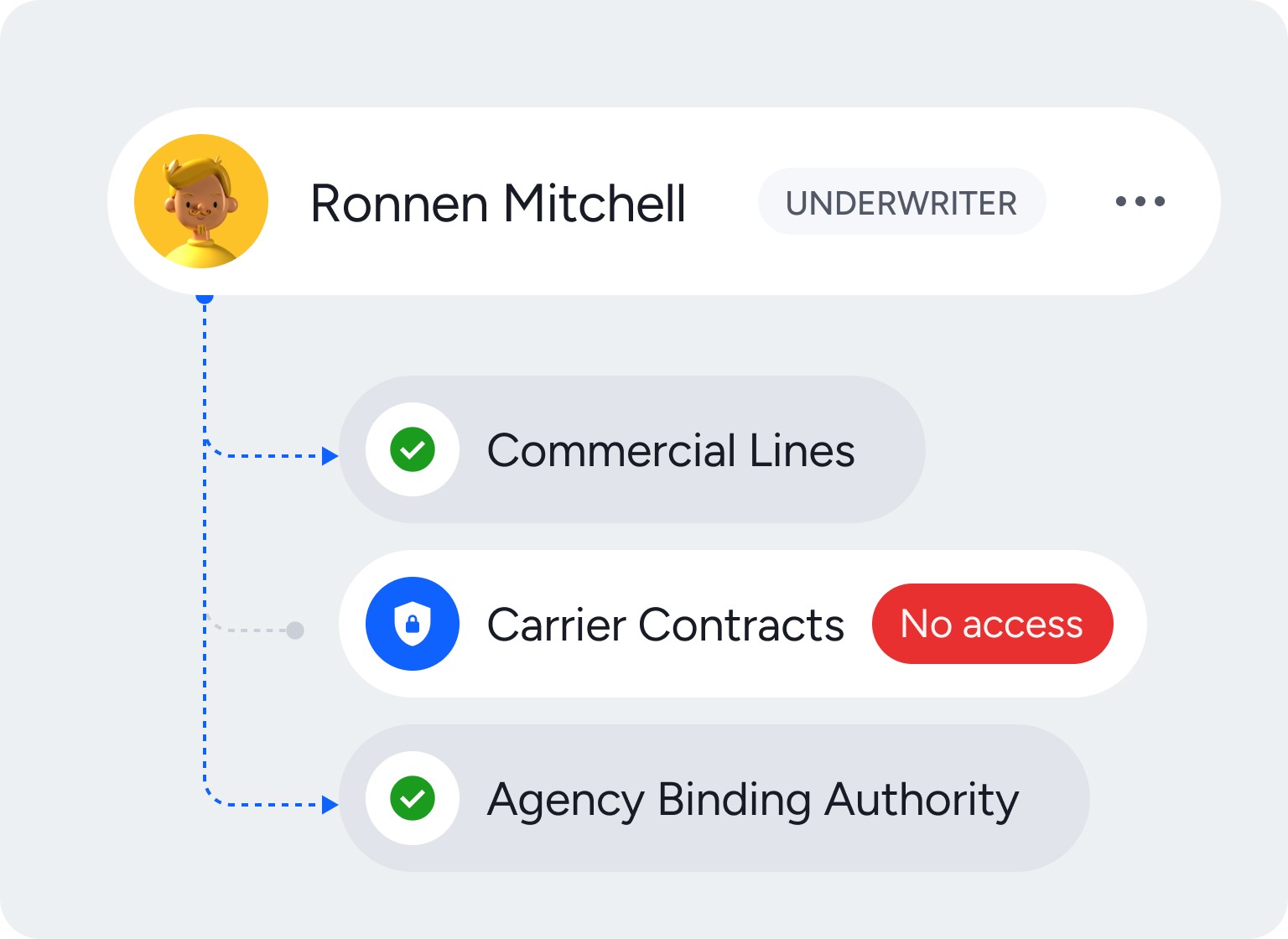

Role-based access for better management and security.

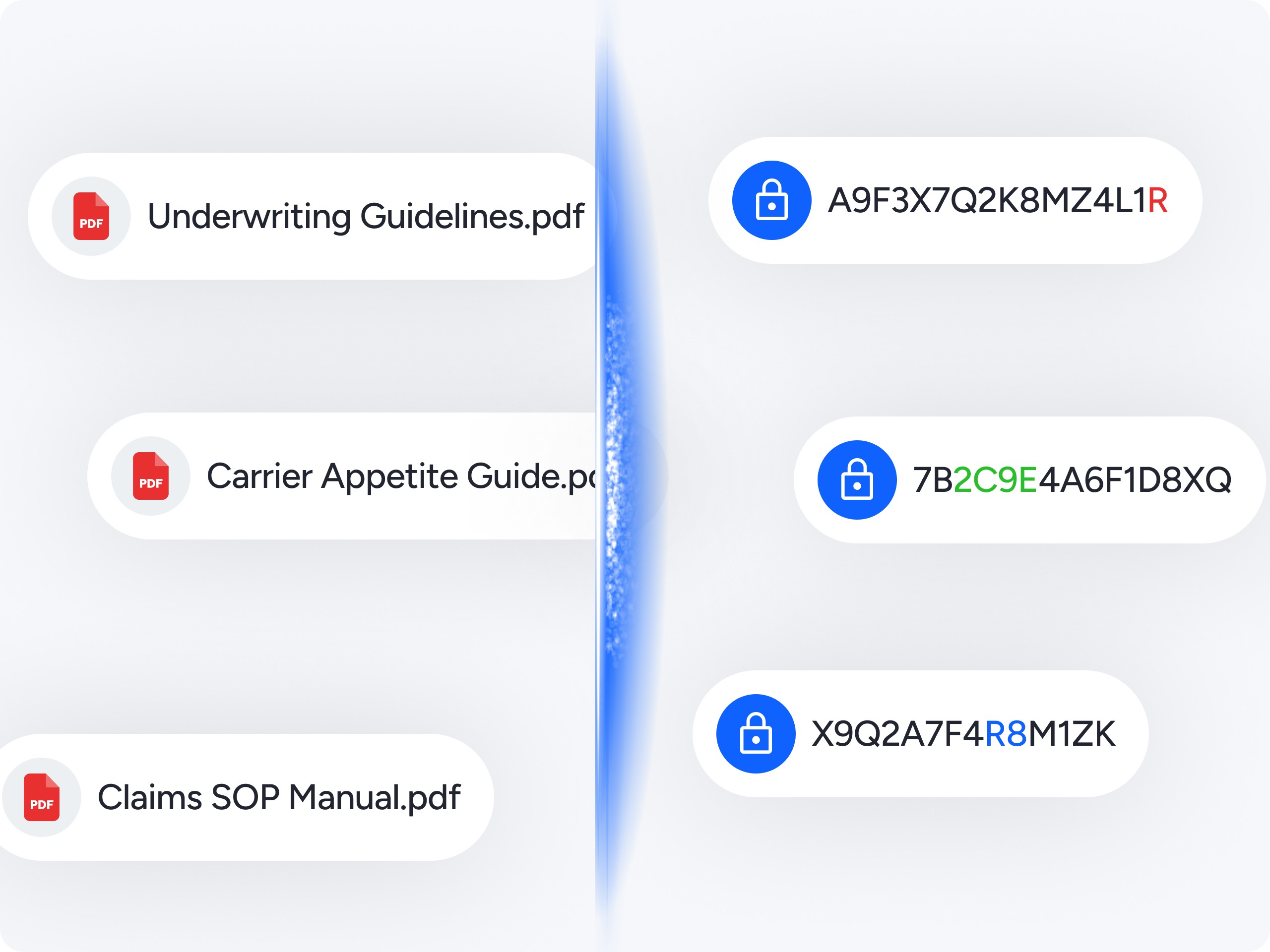

Security first infrastructure

Centralized appetite rules

Bring appetite guidelines, class codes, territory rules, and carrier requirements into one reliable source.

Ask questions in plain language

Ask questions naturally and get clear answers, no training or special prompts required.

Citable, explainable answers

Role-based access and control

Control who sees what, Junior Underwriters, Senior UWs, and leadership get appropriate access levels.

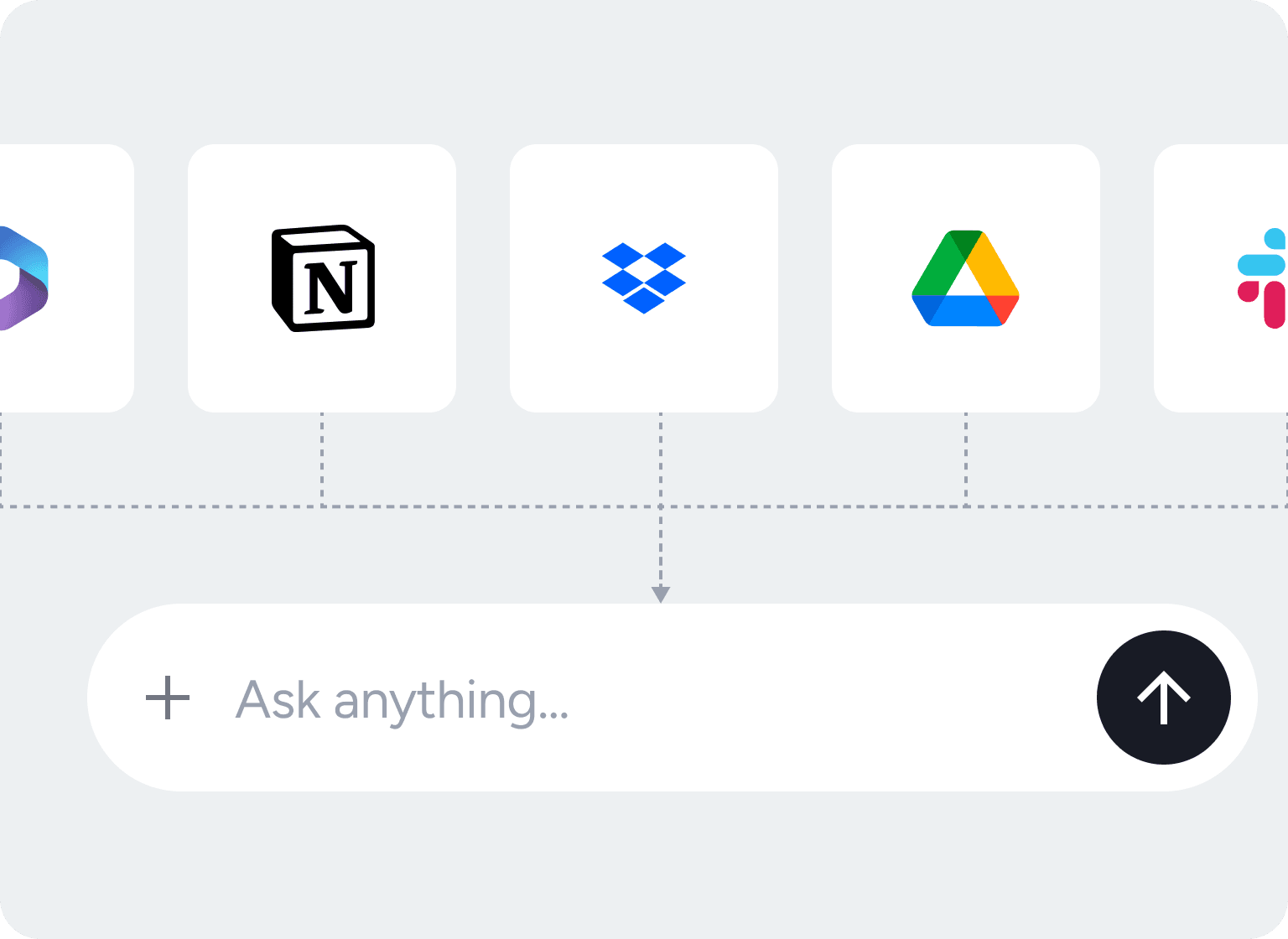

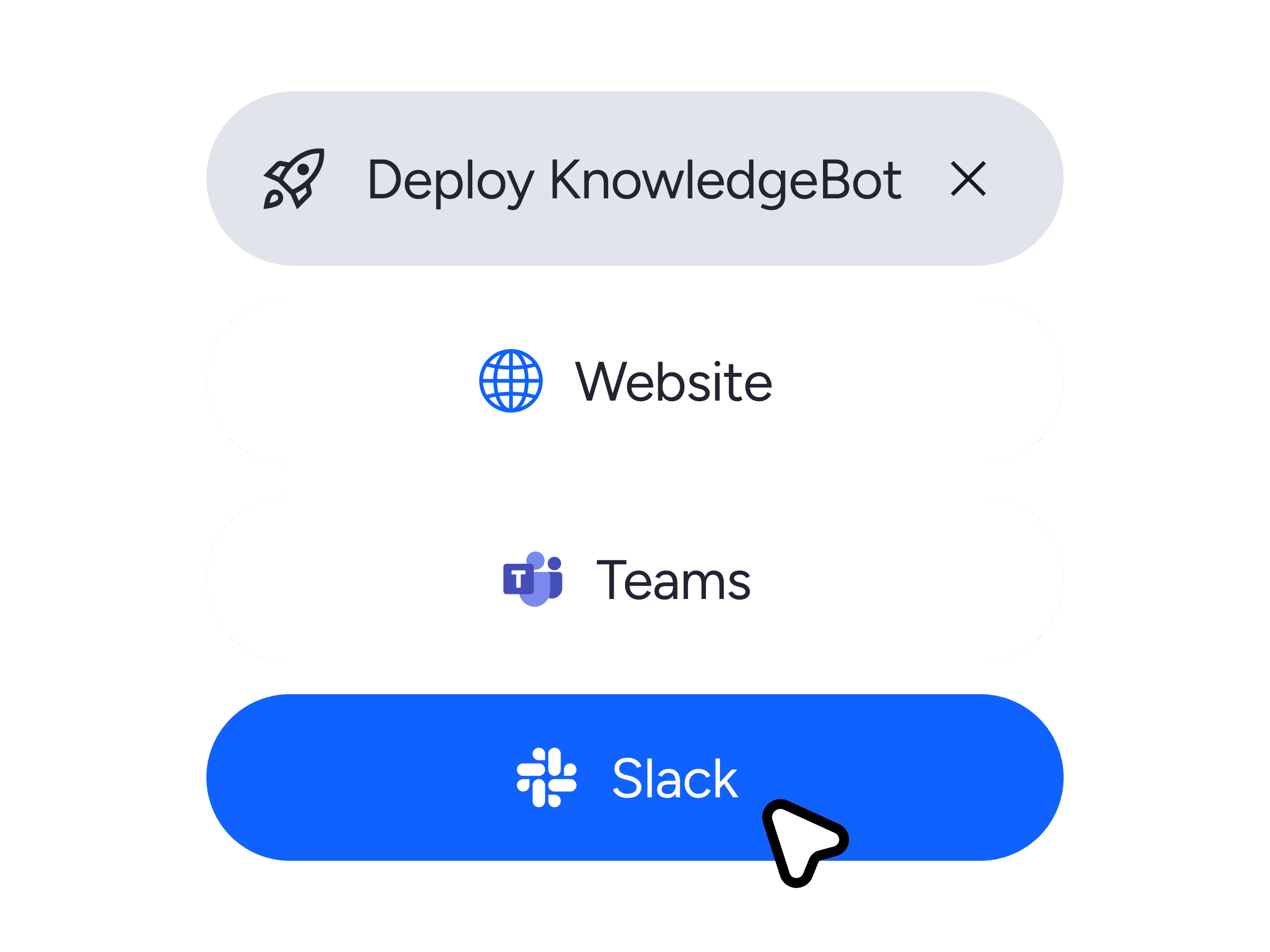

Fast setup with minimal disruption

Deploy to your team via Microsoft Teams, Slack, or a dedicated web portal, live in weeks, not months.

Turn scattered knowledge into

instant, trusted decisions

Discover how underwriting teams reduce triage time, improve consistency, and scale decision-making without increasing risk.

Designed for every role in your firm.

Our AI agent delivers value differently depending on how you work, without changing your existing systems.

Owners and Managing Partners

Reduce E&O exposure and operational risk while improving underwriting consistency and scaling capacity across the organization.

Operations & Compliance Teams

Maintain audit readiness with verifiable, documented decisions. Clear data boundaries and controlled access for regulatory confidence.

Underwriters and Submission Teams

Get instant, reliable answers about appetite, class codes, and guidelines. Spend less time searching and more time on deals that matter.

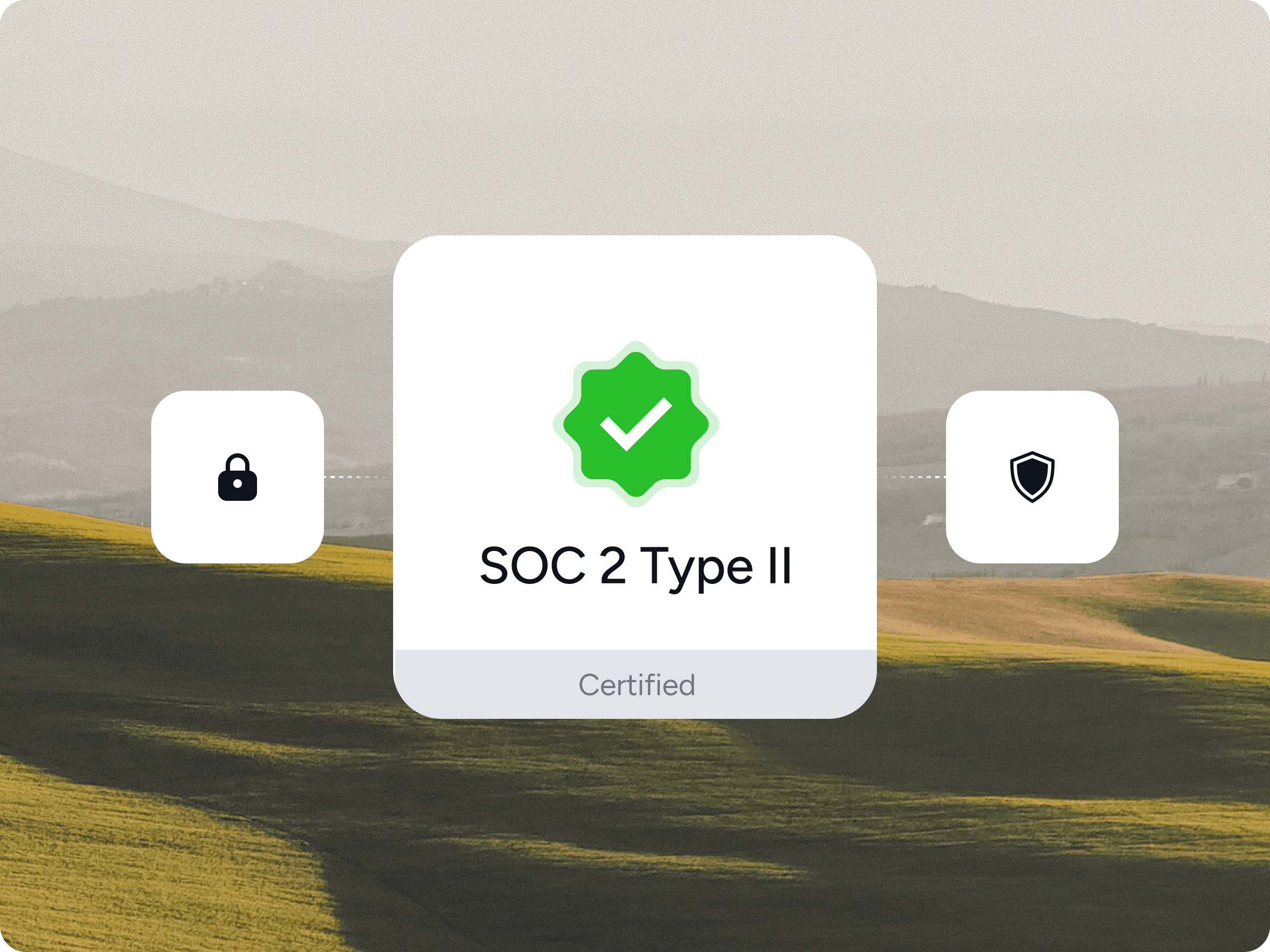

SOC 2 Type II compliant architecture

Private cloud isolation

Role-based access controls

No model training on your data

3x

Faster submission triage

70%

Reduction in time spent searching guidelines

100%

Audit trail on every decision

Frequently asked questions.